>>/462023/

mp3-файл - это аудио-версия статьи.

Продолжение:

The government made two other big moves. In December it devalued the peso by over 50% to partially close the chasm between the official exchange rate and the black-market one. Yet that pushed up inflation. So did interest-rate cuts in December. Normally central banks raise rates to fight inflation. The bank’s rationale was that cutting rates would reduce interest payments on its own bonds, shrinking the amount of money circulating. Inflation initially shot up to a monthly rate of 26% in December. That hurt Argentines, but supercharged Mr Milei’s blender.

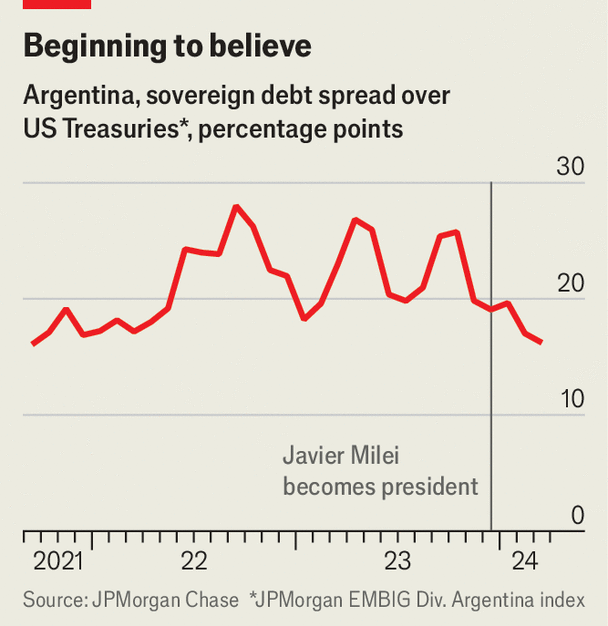

The government says its results vindicate its tough choices. On top of monthly fiscal surpluses and falling inflation, the gap between the official and black-market exchange rates is now only about 20%. Foreign reserves have grown by over $7bn. And the government successfully extended the maturity of stacks of peso debt, reducing pressure on the treasury. The IMF is pleased; markets are starting to believe. Argentina’s country-risk index, a measure of the chance of default, has dropped reassuringly (see chart). On the economy, Mr Milei deserves an eight or nine out of ten, enthuses Andrés Borenstein of Econviews, a consultancy in Buenos Aires, the capital.